Approximately 96% of personal injury cases are resolved out of court through negotiations and settlements, with only about 4% ever proceeding to a formal trial.

Basically, Personal injury collection is the process where the provider treats you now and gets paid later, not from your wallet, but from whatever settlement or verdict comes out of your case. Instead of billing your insurance or handing you a bill at checkout, the provider files a medical lien against your future personal injury settlement. No money changes hands until the case actually resolves, whether that’s through a settlement, a judgment, or a verdict.

Imagine A patient walks into a clinic after a car accident without any insurance money coming through, agrees to treatment on a promise to pay later, only to find that eighteen months later, there is no check, Medical bills after injury keep coming in, and phone calls from a billing office have turned from reminders into threats. This is the situation today. When no one is able to explain how it works, personal injury collection is a process that is often confusing and frustrating for patients, attorneys, and providers alike, and that operates on a different timeline than just about any other kind of medical claim’s billing.

Understanding it from the first personal injury claim to the final personal injury settlement is the difference between a provider getting paid in full and a provider writing off six figures in unpaid care.

Let’s take a look further…

Why is Personal Injury Collection Complex?

There’s no predictable, insurance-claim-to-payment billing path to follow when dealing with personal injury billing. A handful of factors make it uniquely difficult:

- The provider does not have control over the outcome of the case, and payment for the case is based on that.

- Health insurance, Auto insurance, Medicare/Medicaid, and the liability insurance company of the at-fault party all may have an interest in the same claim.

- The purpose of documentation is to meet medical billing requirements as well as legal evidentiary requirements because the records can be used by adjusters, attorneys, and possibly a jury.

- Liens need to be properly filed, monitored, and negotiated, or the provider could lose priority in the payment sequence.

- There are no guarantees with Personal injury claim settlement timeline; the time to get a settlement for a personal injury case varies from a few months to years, depending on the issue of liability, the length of treatment, and litigation

That is why generic medical billing employees frequently do not manage to handle personal injury case volume. It’s a different skill set: knowledge of lien law, understanding the attorneys’ workflow, and patience for a reimbursement process that is different from A/R aging.

How Claim Collections Work in PI Cases: The Full Timeline

Let’s take a look at this step by step

Step 1: The Injury and Initial Treatment

It begins the day a patient is injured as a result of someone else’s carelessness, such as a car accident, slip-and-fall, or workplace accident where a claim is considered personal injury. The patient goes to an urgent care, ER or specialist. If they don’t have health insurance or they opt out of it, the provider may agree to treat them with a Letter of Protection (LOP) that initiates the entire personal injury collection process.

Step 2: Hiring an Attorney and Filing the Personal Injury Claim

Most patients bring on a personal injury attorney early, sometimes within days of the incident. The initial steps by the attorney are to inform the insurance company of the party who was responsible for the accident and to officially start the personal injury case. This is also the time when the attorney usually contacts treating providers to finalize lien agreements and will start to request records as treatment is administered.

Step 3: The Medical Lien Is Filed

Once treatment begins under an LOP, the provider perfects a medical lien, the legal claim that guarantees repayment from the eventual settlement. The correct filing of the lien within time limits, which varies by state, is a crucial part of medical lien on settlement and if that isn’t done, the provider may not have a priority claim for any funds that are paid out. Two or more providers, such as surgeons, physical therapists, and imaging centers, can have separate liens on the same case.

Step 4: Treatment Continues Until Maximum Medical Improvement (MMI)

The patient continues care until they reach MMI — the point where a doctor determines further treatment won’t meaningfully improve their condition. The duration of this phase may vary from a few weeks for soft tissue injuries to more than a year for surgeries and extended rehab. Delayed payment personal injury claims are the norm, not the exception, because provider lien collections are open and continue to build up during this entire time.

Step 5: The Insurer May Request an Independent Medical Exam (IME)

Before agreeing to any settlement figure, the at-fault party’s insurer often requires the patient to undergo an Independent Medical Exam, a second opinion performed by a doctor of the insurer’s choosing. This step is in place to ensure the injury and the treatment were appropriate and necessary and can extend the process by a few weeks.

Step 6: The Demand Package Is Compiled and Sent

Once treatment concludes, the attorney assembles a demand package: complete medical records, itemized bills, lost wage documentation, and a specific settlement figure that the attorney is requesting. Accurate, well-coded records from Step 1 through Step 4 matter enormously here, sloppy documentation at the provider level weakens the demand and can shrink the personal injury settlement the attorney is able to negotiate.

Step 7: Negotiation Between the Attorney and Insurer

The insurer then makes a counteroffer, which is then back and forth, with negotiation sometimes taking weeks and sometimes months. When liability is called into question or the injury is severe, negotiations may come to a complete halt and head toward litigation.

Step 8: Litigation, If Necessary

When negotiation fails to produce a fair settlement, the attorney files a lawsuit. This changes the personal injury lawsuit timeline because mediation or arbitration is often tried first and, if that doesn’t work, the case moves on to trial. This is the part of the process where some cases can drag on for more than two years, especially if the fault is in question or damages are high.

Step 9: Settlement or Verdict, Then Lien Resolution and Disbursement

Once a settlement is reached or a verdict is reached, funds are deposited into the attorney’s trust account. This is the last, and most closely watched, step in personal injury debt collection: the liens are reviewed, and, if necessary, negotiated down, and then the medical liens are settled, usually paid to the attorney before any government payers such as Medicare or Medicaid, before the final payment to the patient.

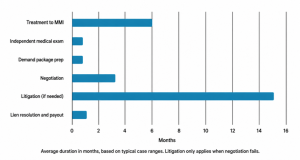

PI Collection Timeline by Stage

Litigation is the biggest swing factor here; most cases settle without ever reaching that stage, which is why total timelines vary so much from one personal injury case to the next.

A straightforward soft tissue injury for which it is clear that there is a liability issue could go from first claim to final settlement in less than a year, while a contentious or severe injury claim could take two years or more once litigation enters the picture. That’s the reason why providers with an A/R cycle of 30-60-90 days or less are not suited to the practice of a lien management system.

This is the backbone of the personal injury claim timeline, personal injury lawsuit timeline, and injury lawsuit timeline that patients and providers both ask about.

What Are Personal Injury Liens?

A medical lien is a legal claim that entitles a health care provider to be paid a portion of the funds from a personal injury settlement before the patient gets paid. The provider does not bill the patient or wait on the traditional insurance, but has the patient’s approval, in the form of a Letter of Protection, and is reimbursed upon the resolution of the case.

Medical lien management involves several moving parts:

- Properly documenting and filing the lien so it’s legally enforceable

- Tracking case status through the attorney’s office

- Responding to lien reduction requests once settlement is reached

- Coordinating with other lienholders (health insurers, Medicare, Medicaid, workers’ comp carriers) who may also have a claim on the same funds

Provider lien collections are generally in the middle of the payout order, but not before attorney’s fees or after the patient’s own recovery, but before, depending on state law and the kind of lien being collected. This is also where delayed payment personal injury claims bring the most conflict. It is a natural and customary part of the process that a provider may wait a year or more only to have the final lien determination negotiated down as part of the settlement, not a bad deal.

Do I Need to Make Payments on Medical Bills Before Settlement?

In most personal injury collection cases treated under a medical lien or Letter of Protection, the patient does not need to make payments before settlement. The provider agrees to wait to get paid until the case is resolved in exchange for the lien. However, patients using their own health insurance or Medicare/Medicaid alongside a pending PI case may still receive statements, since those payers often expect reimbursement from legal settlement through subrogation rather than deferring the bill entirely.

Will My Personal Injury Attorney Negotiate My Personal Injury Bills?

Yes. Medical liens and bills are negotiated down routinely at the time of settlement. This is standard practice and doesn’t reduce the attorney’s fee lien negotiation is done for the client’s benefit, to maximize what they take home after providers, insurers, and government payers are satisfied.

Which CPT Codes(Current Procedural Terminology) are Used for Car Accident Injuries

Accurate CPT codes personal injury collections are critical because insurers and opposing counsel scrutinize documentation closely.

Common CPT and HCPCS codes medical billing teams work with include:

|

Code |

Description |

|

99202–99215 |

Evaluation and management (E/M) visits, new and established patients |

|

72040–72110 |

X-rays of the spine (cervical, thoracic, lumbar) |

| 97110 | Therapeutic exercise |

| 97140 | Manual therapy techniques |

| 98940–98942 | Chiropractic manipulative treatment |

| 20610 | Joint injection, major joint |

| 72141–72158 | MRI of the spine |

| S9083 | HCPCS code for global fee, case-rate treatment sometimes used in PI billing |

Correct CPT and HCPCS code selection, paired with clear documentation of medical necessity, directly affects both claim approval and the final settlement valuation that an attorney can negotiate.

How to Negotiate a Bill in Collections: What Actually Moves the Number

Medical bill negotiation in personal injury collections cases happens at two points: when the lien is filed, and again once settlement funds are available. Effective negotiation typically involves:

- Auditing the original bill for duplicate charges or coding errors before it’s disputed

- Comparing billed amounts to usual, customary, and reasonable (UCR) rates for the region

- Presenting the total lien burden across all providers, since insurers and attorneys often negotiate more aggressively when multiple liens are stacked

- Offering a reduced lump-sum payoff in exchange for faster resolution

Unpaid Medical Bills Lawsuit and Debt Collection in a Personal Injury Case

As for those personal injury cases that stall or where the provider isn’t involved in a lien arrangement, unpaid balances can be placed in traditional collections, which may even lead to an unpaid medical bills lawsuit against the patient. This is where the personal injury debt collection industry meets the consumer protection law, and there are some precautions to take.

Debt collection in a personal injury collection context is still governed by the Fair Debt Collection Practices Act (FDCPA), which requires collectors to:

- Send a written validation notice within five days of first contact

- Avoid harassment, threats, or misleading statements about the debt

- Stop collection activity on disputed accounts until the debt is verified

- Respect the patient’s communication preferences and quiet hours

Because personal injury collections accounts involve protected health information. HIPAA rules apply on top of the FDCPA, which means collections while case pending settlement. Require extra documentation discipline compared to standard consumer debt.

2026 Regulatory Updates Affecting Personal Injury Collections

A few developments from 2026 are directly relevant to anyone managing PI billing services and collections right now:

- The CFPB’s January 2025 rule that would have removed most medical debt from consumer credit reports was vacated by a federal court in July 2025 for exceeding. The agency’s authority under the FCRA after the CFPB issued the rule amending Regulation V on January 7, 2025. Prohibiting creditors from considering medical debt and barring credit bureaus from including it on reports. As of 2026, that federal ban remains stalled in litigation.

- Despite the federal rollback, the three major credit bureaus still voluntarily remove paid medical collections regardless of balance. Drop unpaid medical collections under $500. And apply a 12-month grace period before medical debt appears on a report, and roughly 15 states have passed their own laws adding protection against medical debt credit reporting beyond federal requirements (Credlocity, updated May 2026).

- California, New York, Illinois, Colorado, and Washington rank as the five most complex state compliance environments for collections in 2026. And most states now require collection agencies to hold active state licensing. With unlicensed collection potentially rendering the debt unenforceable (MSB, 2026 State Scorecard).

- On the medical lien side, some states have begun passing legislation to limit how insurance companies file liens or to streamline negotiation timelines, aimed at reducing the years-long waits some plaintiffs face for their share of a settlement (Wallace Miller, 2026).

With the constantly changing landscape, providers and billing teams are advised. To check the rules for the current situation on the CFPB’s regulatory site (consumerfinance.gov) and their state. Attorney general’s office before finalizing their collection policy.

PI Billing and Collections: In-House vs. Outsourcing PI Billing & Collections

Handling personal injury billing and collections in-house is possible, but it demands dedicated staff. Who understand lien law, attorney communication, and long-cycle A/R management. Resources many practices don’t have spare capacity for. This is why outsourcing PI billing & collections has become a common. Move for practices with a growing personal injury collection caseload.

Choosing a PI billing partner comes down to a few criteria:

- Proven experience specifically with personal injury case types, not just general medical billing

- A documented process for medical lien management and provider lien collections

- Transparent reporting on aging claims and settlement status

- Compliance infrastructure that satisfies both FDCPA and HIPAA requirements

- Direct coordination capability with attorney offices, since most delays trace back to missing documentation or slow demand-package turnaround

Revenue Cycle Management for PI Cases: What Good Looks Like

Strong revenue cycle management for personal injury cases isn’t just about filing a lien and waiting. It includes:

- Verifying coverage and liability sources before treatment begins

- Coding accurately from the first visit, since early documentation shapes the entire claim

- Maintaining consistent communication with the patient’s attorney throughout treatment

- Auditing liens before settlement to catch errors that would otherwise shrink the payout

- Tracking every case against expected settlement timelines to flag stalled claims early

Final Thoughts

Personal injury collection is slow by design, legally layered, and unforgiving of documentation gaps. But it doesn’t have to be a black hole for practice revenue. Providers who understand the lien process. Have a solid in-house PI billing team or contract with one, and code correctly from day one. And make sure they get paid when they’re due are the ones who get paid. And they don’t do so at the expense of their practice sitting on a settlement.

Frequently Asked Questions

1. What is the typical timeframe for a personal injury settlement?

In most cases, the cases are resolved within 6 months to 2 years after the injury. Depending on how long the treatment takes, whether a lawsuit is needed, and if there is a dispute over liability.

2. What’s the difference between a personal injury claim and a personal injury case?

A personal injury claim is the legal document filed with an insurance company. A personal injury case is the actual case itself. It is possible that a case may not be a lawsuit if the claim is resolved without litigation.

3. Will a personal injury collections provider recover from the loss of a case?

This is contingent on the agreement. Many Letters of Protection say that if the case does not settle. Then the patient may be liable for the remainder via normal billing practices.

4. If there is more than one on a settlement, what happens?

Typically, liens are paid in order: attorney’s liens are paid first, then Medicare, Medicaid, and then other medical liens. However, the order of paying varies from state to state.

5. How do I negotiate a bill that’s already gone to collections?

Start by requesting an itemized statement and comparing it against your treatment records. All errors and duplicate charges are common. From there, either your attorney or a billing negotiator can present your total lien burden across all providers and propose. A reduced lump-sum payoff. Which collectors often accept in exchange for faster, guaranteed payment.

6. If my health insurer already paid some of my bills, do they get reimbursed from my settlement?

Yes. This is called subrogation, your health insurer, Medicare, or Medicaid can claim reimbursement. From your settlement for anything they already paid toward your accident-related treatment. And that claim is typically factored in alongside any medical liens before you receive your net check.

7. Do I need a personal injury collection attorney to negotiate my medical bills, or can I do it myself?

You can negotiate directly with providers, but most people work with a personal injury attorney. Because they already have lien relationships and negotiating leverage that most patients don’t. Whether you’re working with an attorney locally, a personal injury attorney in Denton, TX, for example, or elsewhere. This negotiation is a standard part of what they handle as your case moves toward settlement.

8. What happens if my settlement isn’t enough to cover all my medical bills?

This is one of the most common outcomes in personal injury cases, not a rare exception. When settlement funds fall short of the total lien amount, your attorney typically negotiates each lien down proportionally. So you still walk away with something, rather than the first lienholder. Taking the full settlement and leaving nothing for the rest.