Personal injury is something you can never be prepare for, it can happen to you out of nowhere. Basically, personal injury is when you get injured because of someone else’s actions or negligence.

If another person, company, or organization causes you harm and could have reasonably prevented it, you may have the right to seek compensation for your injuries and related losses.

If you own a medical practice and receive calls from patients who have been in a car accident, workplace injury, or slip-and-fall accident, you have most likely heard the term you have most likely heard the term “medical billing for personal injury cases”. However, it’s not the same as traditional medical billing, and you’re probably losing money if you’re working with these patients without knowing what you’re doing. You have most likely heard the term medical billing for personal injury cases; its process is a specialty revenue stream that most healthcare providers can’t do effectively. That is why many physicians miss thousands of dollars annually.

This guide is designed to change that and explain to you why personal injury billing is important and exactly how to manage it effectively.

Why Personal Injury Billing Matters for Your Practice?

However, in the case of personal injury claims, things are quite different. They are unlikely to be able to afford treatment without it being covered by their health insurance plan, and their insurance won’t pay for injuries that were caused by someone else’s negligence.

Instead, this is what happens: A patient is injured during an accident. They employ a personal injury claims lawyer. That attorney agrees to represent them on a contingency basis (that is, if the case settles or wins). In this period, the patient must receive medical treatment. They come to you. However, they don’t have any cash to spare at the moment.

This is where personal injury billing comes in.

Understanding the Basics: What Personal Injury Billing Actually Is?

So, what is personal injury billing? Personal injury medical billing refers to documenting, coding and billing of the medical care that is provided to patients who have suffered an injury as a result of another party’s wrongdoing or negligence. The payment is not from the patient’s insurance or from their wallet, but from the settlement or judgment obtained in their case.

The money that comes when a personal injury case settles doesn’t necessarily go to everyone equally. It is distributed in a certain sequence. Your doctor’s bills are paid first (sometimes). The attorney collects their contingency fee (typically, 33% to 40%). The patient is left with what’s remaining.

But here’s the critical part: if you don’t bill correctly and establish a legal claim against that settlement, you might not get paid at all.

The Payment Model: How You Actually Get Paid

Instead of getting checks from insurance within 30-60 days, personal injury medical billing has a different process. Your wages may not be received for 6 months, 18 months or even 3 years. You must have to be ready for that.

It is usually done like this:

1. Treatment Phase: Patient comes to you. You provide care. You take care to record every detail.

2. Billing Phase: You bill the case for the medical services rendered. This goes to the personal injury attorney, not to insurance.

3. Waiting Phase: The case goes through investigation, negotiation, or trial. You wait. Sometimes a long time.

4. Settlement Phase: The case settles. Money arrives.

5. Payment Phase: You finally get paid, but only if you filed a proper lien or billing statement.

The biggest mistake healthcare providers make is not billing the case at all. They treat the patient without documenting it properly for the personal injury case, and then when the settlement comes, they miss out entirely because they have no legal claim to the funds.

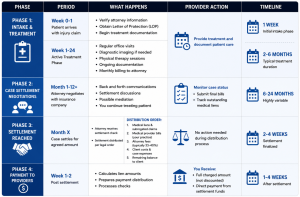

Personal Injury Billing Timeline & Process Flow

Here’s a visual breakdown of the entire payment cycle and timeline you can expect:

TOTAL TIME FROM TREATMENT TO PAYMENT: 8 months to 3+ years

Key Takeaway: You must have systems in place to track these cases through every phase. Many practices lose money because they don’t follow up once treatment ends. The attorney has your bills. The case settles. But if you haven’t documented properly or sent final billing, you get nothing.

What is a Letter of Protection (LOP): Your Safety Net

A letter of protection in personal injury billing is a pledge. The personal injury lawyer guarantees to cover your medical expenses with the settlement funds. It helps protect you by establishing a legal commitment. If the patient has a personal injury case, he/she should come in with an LOP from their attorney. This letter says: “I will ensure this provider is paid for treating my client before I take my fee.”

If you do not have an LOP, that means you are essentially prescribing the patient on a credit basis, without any guarantee of payment. An LOP gives you the legal means of recourse in the event the attorney doesn’t pay you.

Here’s what a solid LOP includes:

- Patient’s full name and case details

- Attorney’s name and contact information

- A promise that your medical bills will be paid from the settlement

- Confirmation that this is a legitimate personal injury case

- The attorney’s signature

If a patient comes to you claiming to have a personal injury case but can’t produce an LOP, that’s a red flag. Call the attorney’s office to verify. Seriously. Don’t skip this step.

Difference Between Personal Injury Billing and Regular Medical Billing

Your billing staff probably knows how to handle insurance claims. They know coding, claims submission, and appeal processes. But personal injury billing for providers has different rules.

Insurance Billing

You are billing insurance companies. They have contracted rates. They refuse to accept claims for stated reasons. Appeals are made in accordance with procedures. Payment period is transparent.

Personal Injury Billing

You get to bill at the usual rate, NOT the insurance discounted rate. A “payer” is a future settlement. No DENY codes for insurance. The process is totally unpredictable. You might need to establish a proper PI lien collection if the attorney won’t cooperate.

Another major difference: insurance companies consider medical needs and appropriateness. They wonder if you actually needed the treatment(s). The focus in personal injury cases is too different. Medical requirements of the injured party are less subject to questioning, as it is well documented and liability is clear.

However, it is necessary to bill correctly. Excessive billing or unneeded treatment may be a problem in settlement negotiations or in a trial. Your bills will be closely reviewed by the defense.

|

Above is the chart that completely defines that why is personal injury billing different from regular medical billing.

Can Health Insurance Be Used for Personal Injury Cases?

This is where most of the providers become confused about how Insurance Interacts with personal injury cases?

The answer is “yes” and “no, it’s complicated.”

Numerous health insurance policies have a condition on personal injury liability. In other words, insurance companies are saying: “If you get hurt when someone else is legally responsible, then we will cover your medical expenses, but we are entitled to be reimbursed from the settlement this is called subrogation.

Let’s say, for example, That patient gets hit by a car. They receive $15,000 for treatment and follow-up at the ER through their health insurance. Later, the case settles for $100,000. The insurance company says that they deserve to recover $15,000 from the settlement that’s the subrogation amount.

Now the fun begins, as you, the provider… If the insurance company has already paid for the insurance for the care, do you bill the case? In general, no, first bill insurance. They pay. The lawyer conducts negotiations with the insurance company’s subrogation claim.

However, if the insurance company refuses to cover the patient or the patient does not have insurance, then it is a personal injury case, and you invoice the lawyer.

Most practices have a mixed bag of reality. For some patients, there is coverage under their insurance plan. Some don’t. Before commencing treatment, one should have protocols to determine which is which.

Medical Coding in Personal Injury Cases: Getting It Right

Your coding department must realize that personal injury cases are coded much like any other medical case, but the diagnosis codes are very important.

Diagnosis codes MUST be using to provide a clear record of the injury. For personal injury cases, ICD-10 coding needs to include the following information:

- The exact type of injury (fracture, strain, contusion, etc.)

- The area of the body that is affected.

- The external cause (V codes for vehicle accidents, W codes for falls, etc.)

- The episode of care (initial encounter, subsequent visit, sequela)

The documentation is critical as it provides a ground for medical necessity and the causation between the incident and the medical services rendered. There is no need to change the coding when billing for services; the CPT coding is the same as usual. What is changing is the level of documentation and coding of the diagnosis side. For example, someone who has had a car accident has neck pain and a headache.

Rather than coding it generically, you’d code:

- M54.2 (Cervicalgia neck pain)

- R51.9 (Headache, unspecified)

- V43.92XA (Car occupant, injured in collision with car, initial encounter)

That final code, the external cause code, is what connects the treatment to the accident. It’s essential for personal injury medical billing.

Building an LOP-Based Billing System

If you want to profit from personal injury cases, you need systems. Here’s what works:

Front Desk Protocol

When scheduling patients, ask if they’re being treated for an injury related to an accident or incident. If yes, ask for the attorney’s information.

Verification Process

Before the patient’s first appointment, call the attorney’s office. Confirm the case exists. Request an LOP. Get it in writing.

Documentation Requirements

Train your clinical staff to document the injury mechanism clearly. Don’t just write “patient reports neck pain.” Write “patient reports acute onset of neck pain immediately following a motor vehicle accident where the patient was struck-up from behind.”

Coding Standards

Use external cause codes consistently. Make sure diagnosis codes reflect the injury clearly.

Billing Procedures

Bill with LOP in hand. Include your standard fees. Don’t inflate charges trying to maximize the patient’s settlement collection cause it backfires.

Follow-up System

Track which cases have active LOPs. Periodically contact attorneys for case updates. When settlements happen, submit final bills promptly.

Are there Any Challenges in Personal Injury Billing?

Let’s be real about the headaches you’ll encounter.

Delayed Payments

Cases don’t settle on your timeline. A patient may be treating for months, and then it may take two years to get paid. This puts cash flow under stress. There are many practices that may need patients to pay a little bit out of pocket or manage this in some other way.

Non-Cooperative Attorneys

Some attorneys are difficult to reach. They lose LOPs. They delay responding to billing inquiries. Building relationships with reputable attorneys in your area helps, but you’ll still encounter difficult ones.

Insurance Complications

When insurance is involved, coordination gets messy. Insurance subrogation claims, coordination of benefits, and coverage questions create an administrative burden.

Disputes Over Medical Necessity

Defence attorneys sometimes challenge whether all your treatment was necessary or reasonable. Your documentation needs to be bulletproof.

Collection Issues

Some lawyers don’t pay even after a settlement. Collection may be needed or a medical liens placed on the case. This means that there must be legal engagement and investment of funds.

Should Medical Practices Outsource Personal Injury Billing?

There are lots of benefits of personal injury billing services. A lot of practices choose to outsource personal injury billing for patients because it’s too complicating to be manage in-house. They don’t know what to do. The case tracking requirements are challenging. It results in cash flow issues due to the delayed payment cycles.

When you take a look at the benefits of personal injury medical billing services, that’s exactly when outsourcing makes sense.

A specialized personal injury billing company:

- Manages all LOP verification

- Handles coding and billing compliance

- Tracks case statuses

- Pursues collections

- Manages lien processes

- Provides reports on pending cases

Typically, you’ll pay it as a percentage of your collections. Many practices feel that the percentage that they receive is good value for what they would have to bring in-house.

For individuals who are seeing less than 5-10 personal injury cases per month, outsourcing can be a financial option. If you have more than 20 per month, you may want to consider having it in-house for personal injury billing for patients.

Compliance and Documentation: Protecting Yourself

Many people ask: how does personal injury billing work?

Healthcare providers sometimes grow anxious about these cases due to compliance concerns. They shouldn’t be also they should provide you adhere to normal medical and billing procedures.

No special or risky things are being done. You have an injured patient. You’re coding and billing appropriately. The only difference is the payer source (settlement as opposed to insurance).

What you need to avoid:

- Don’t agree to charge inflated rates just because it’s a personal injury case

- Don’t order unnecessary tests to maximize the bill

- Don’t document treatment that didn’t happen

- Don’t bill for services not rendered

- Don’t waive copays or deductibles as a favor to attorneys (though some patients genuinely can’t pay)

Your documentation and billing should be identical,

whether it’s a personal injury case or an insurance case, the services are real. The treatment is medically necessary. The coding is accurate. That’s it.

The Bottom Line

Don’t let personal injury billing intimidate or scare you. It’s a legitimate and possibly rewarding source of income for healthcare providers. The patients require treatment. They’re injured. Someone’s liable. Funding will be provided through settlement.

Your job is to treat them appropriately, document clearly, code accurately, protect yourself with an LOP, and follow up on payment. Although it’s not an easy process, here you have the complete guide to personal injury billing and PI lien collection to do those things correctly and consistently

However, outsourcing takes almost 90% off your workload, and you’ll find that personal injury cases become a reliable part of your practice revenue.

The ones that are going to struggle are the providers who are treating without protection, billing without proper documentation and the ones that give up after the first challenging case. Those who do succeed are systematic. They have systems, they hire experts to do their work and understand the rules.

Now you have the knowledge of the rules. Now it’s time to develop those systems.